Global In-Flight Catering Services Research Report 2025 (Status and Outlook)

Report Overview:

In-Flight Catering Services provide prepared meals, beverages, and related hospitality offerings to airline passengers during flights. These services encompass meal planning, production, packaging, and delivery to aircraft, ensuring food safety, quality, and compliance with airline standards. Modern in-flight catering goes beyond basic meals to include premium dining experiences, special dietary accommodations, and branded offerings tailored to passenger preferences and airline positioning. Efficient logistics, strict hygiene protocols, and menu innovation are essential to delivering a seamless onboard experience. By enhancing passenger satisfaction and reinforcing airline branding, in-flight catering has become an integral part of airline operations worldwide.

The global In-Flight Catering Services market is currently at a critical transition stage, moving from post-pandemic recovery toward structural growth and high-quality development. In 2025, the global market size reached USD 22.263 billion and is projected to expand to USD 34.181 billion by 2035, growing at a CAGR of 4.38%. The industry is characterized by a multi-layered transformation driven by demand recovery, structural upgrading, and capability reconfiguration. On the demand side, the rebound in global air passenger traffic—particularly the recovery of international and long-haul routes—continues to support baseline meal demand, while passenger preferences are rapidly shifting from standardized offerings toward healthier, more personalized, and experience-oriented consumption, driving a premiumization and functional upgrade of inflight meals. On the supply side, leading players are reshaping operational models through digital factories, automation, and AI-driven supply chain management to address rising labor costs and increasing SKU complexity, while simultaneously accelerating ESG and sustainability transitions, making carbon management, waste reduction, and eco-friendly packaging key competitive factors.

The global In-Flight Catering Services market is currently at a critical transition stage, moving from post-pandemic recovery toward structural growth and high-quality development. In 2025, the global market size reached USD 22.263 billion and is projected to expand to USD 34.181 billion by 2035, growing at a CAGR of 4.38%. The industry is characterized by a multi-layered transformation driven by demand recovery, structural upgrading, and capability reconfiguration. On the demand side, the rebound in global air passenger traffic—particularly the recovery of international and long-haul routes—continues to support baseline meal demand, while passenger preferences are rapidly shifting from standardized offerings toward healthier, more personalized, and experience-oriented consumption, driving a premiumization and functional upgrade of inflight meals. On the supply side, leading players are reshaping operational models through digital factories, automation, and AI-driven supply chain management to address rising labor costs and increasing SKU complexity, while simultaneously accelerating ESG and sustainability transitions, making carbon management, waste reduction, and eco-friendly packaging key competitive factors.

The core growth drivers of the market stem from the combined effects of air traffic recovery, airline business model restructuring, and digital technology advancement. As global passenger volumes continue to recover—led by international routes and the rapid expansion of Asia-Pacific, alongside increasing long-haul capacity utilization—demand for inflight catering is expanding both in volume and per-flight value. The recovery of airline profitability further strengthens this transmission mechanism, enabling carriers to increase investment in premium and customized catering services, transforming inflight meals from a basic cost item into a strategic tool for brand differentiation and service enhancement. In the competitive landscape, full-service carriers leverage premium dining to reinforce brand value, while low-cost carriers monetize onboard meals as ancillary revenue streams, jointly elevating the strategic importance of catering services. Meanwhile, the expansion of global aviation networks and the rising share of long-haul flights significantly increase meal complexity and value density per flight, further strengthening demand for cold chain logistics and high-end ingredients. At the same time, the rapid adoption of digitalization and artificial intelligence is fundamentally reshaping operations—automation, predictive analytics, and data-driven supply chain management are improving efficiency, reducing waste, and optimizing cost structures, driving the industry’s transformation from a traditional labor-intensive service model toward a more intelligent and precision-driven operational system.

At the same time, the global inflight catering industry is facing multiple structural challenges that create systemic pressure, particularly rising multi-dimensional costs, supply chain fragility, physical operational constraints, business model divergence, evolving demand complexity, and external shock risks. The simultaneous increase in food raw material, labor, and energy costs is compressing the entire value chain, prompting leading companies to rely on automation, AI optimization, and energy efficiency improvements, while smaller players face margin deterioration and consolidation pressure, accelerating industry concentration. The industry’s highly globalized and time-sensitive supply chain means that disruptions at any stage can be amplified into systemic operational risks—for example, sudden supplier changes leading to service degradation, or aircraft delivery delays indirectly constraining market expansion. In addition, strict constraints on aircraft cabin space and weight impose structural trade-offs between meal quality, variety, and cost efficiency. The divergence between full-service and low-cost carriers further increases operational complexity, requiring suppliers to simultaneously manage high-end customized offerings and standardized low-cost production systems. Rapid shifts in passenger demand toward health, personalization, and diversity have significantly increased SKU complexity, pushing the supply chain from standardized production toward highly customized systems. Moreover, the industry remains highly vulnerable to external shocks such as pandemics, geopolitical tensions, fuel price volatility, and airport disruptions, which can directly and disproportionately impact revenue in the absence of demand buffers.

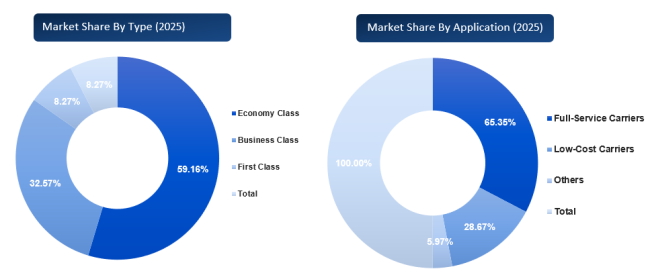

From a cabin class perspective, economy class remains the dominant segment, accounting for 59.16% of the global market in 2025 and growing steadily at a CAGR of 4.30% through 2035, forming the stable foundation of overall demand due to its strong correlation with total passenger volumes. Business class, although smaller in scale (USD 7.252 billion in 2025, 32.57% share), exhibits the fastest growth among all cabin segments with a CAGR of 4.64%, reflecting the recovery of premium travel and increasing demand for high-value catering experiences. First class, while relatively small (USD 1.840 billion in 2025, 8.27% share), continues to grow steadily at 3.92%, supported primarily by ultra-premium route recovery and luxury service demand, though with more limited growth elasticity compared to business class.

From an airline business model perspective, full-service carriers remain the dominant force, accounting for USD 14.55 billion in 2025 and 65.35% market share, with stable growth of 3.91% through 2035, reinforcing their role as the core revenue base of the industry. In contrast, low-cost carriers represent the most dynamic segment, reaching USD 6.383 billion in 2025 with a 28.67% share and the highest CAGR of 5.62%, driven by the rapid monetization of onboard catering through pre-order systems and ancillary revenue models. This reflects a clear shift of inflight catering within LCCs from a non-core service to a structured revenue-generating component.

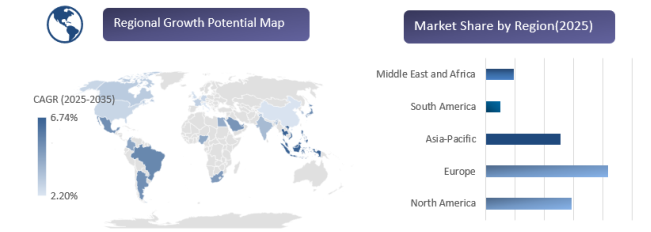

Regionally, the market exhibits a clear divergence between mature and high-growth regions. Europe remains the largest market at USD 8.366 billion in 2025 (37.58% share), supported by dense international route networks, followed by North America at USD 5.858 billion (26.31% share) with stable growth of 3.65%. In contrast, Asia-Pacific emerges as the primary growth engine, reaching USD 5.122 billion in 2025 (23.00% share) and expanding at a leading CAGR of 6.11% through 2035, driven by rapid passenger growth, increasing low-cost carrier penetration, and expanding intra-regional and long-haul connectivity. This positions the region as the most important incremental demand source for global inflight catering services.

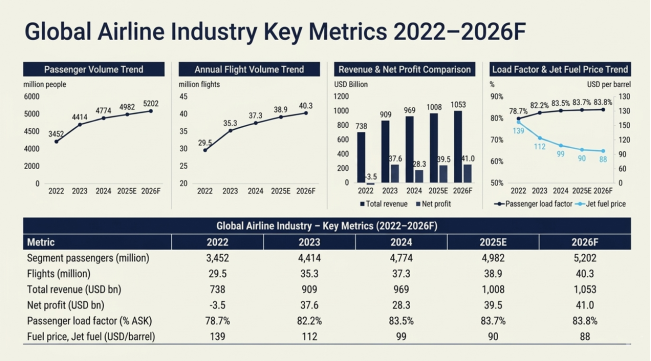

Global Airline Industry – Key Metrics (2022–2026F)

The global aviation industry demonstrated a trend of steady recovery and growth during the period from 2022 to 2026. Passenger volume increased from approximately 3.45 billion in 2022 to about 5.20 billion in 2026, while the number of flights also rose from 29.5 million to 40.3 million. Revenue climbed steadily, growing from $738 billion to $1,053 billion; meanwhile, after recording a net loss of $350 million in 2022, net profits are projected to reach $3.95 billion and $4.10 billion in 2025 and 2026, respectively. Passenger load factors remained at high levels, rising from 78.7% to 83.8%, signaling improvements in airline operational efficiency. Concurrently, aviation fuel prices continued to decline—dropping from $139 per barrel in 2022 to $88 in 2026—thereby supporting cost-control efforts within the industry.

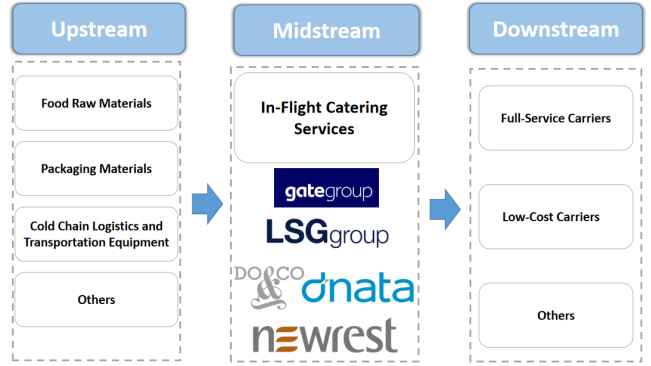

In-Flight Catering Services Industry Chain Analysis

Development Trends

Leading Players Enter High-Growth Trajectory

The period from 2025 to 2026 marks a critical turning point for the in-flight catering industry, as it transitions from a financial recovery phase into a high-growth trajectory. Airline networks that were previously grounded during the pandemic have largely resumed operations, and leading suppliers have delivered consistently improving financial results. SATS reported revenue of SGD 5.8 billion for FY2025, representing a 13.0% year-on-year increase, while net profit after tax surged to SGD 243.8 million—more than quadrupling from SGD 56.4 million in the previous fiscal year. Gategroup posted revenue of €5.61 billion for FY2025, with an EBITDA margin of 8.3%, a significant improvement from 7.5% in 2024. Its net debt‑to‑EBITDA ratio fell from 3.74x to 3.25x. These improvements provide strong evidence of the industry’s balance‑sheet repair over the past few years and have laid a solid financial foundation for subsequent capital actions (e.g., IPOs). DO & CO’s revenue for the first half of FY2025/2026 grew 9.3% year‑on‑year to €1.24 billion. Newrest, through multiple strategic acquisitions, drove its overall performance up 33% to €3.34 billion, with four acquisitions alone contributing €555 million in incremental revenue.

On top of these confirmed growth drivers, leading players have unveiled more ambitious strategic blueprints. After reshaping its financial and operational systems, Gategroup launched its comprehensive strategic roadmap “IGNITE 2030.” The core direction is to consolidate its core in‑flight catering business while expanding horizontally into areas such as onboard retail solutions, thereby diversifying revenue streams and reducing dependence on single catering contracts. Gategroup also changed its reporting currency from Swiss francs to euros, sending a clear signal of the deep alignment between its global business focus and capital structure. Newrest’s management has explicitly stated that new business segments such as remote site management and facility management are expected to approach 50% of consolidated revenue by 2026, marking a systematic expansion of large catering players into highly synergistic adjacent industries.

Digital Transformation

Against the backdrop of rising labour costs and increasingly stringent customer demands for consistency, a new generation of digital production models is redefining industry standards. Newrest opened a 14,000‑square‑meter new automated factory in Madrid, equipped with robotic tray assembly lines, AI‑driven preparation, picking and packaging processes, and precise sales reconciliation systems. It handles 130 flights per day and serves 42 carriers, signalling that the in‑flight catering supply chain has moved from a labour‑intensive model into a new phase of “Industry 4.0 automated production.” Beyond aviation, Newrest continues to drive digital transformation: it deployed its first digital factory at Paris‑Orly Airport in 2023 for a dedicated low‑cost carrier, and in 2025 opened a second digital factory fully focused on the rail sector, replicating and adapting its aviation catering innovation model to rail logistics.

LSG Sky Chefs has similarly recognised automation as a key to managing operational complexity, maintaining consistent quality and reducing labour dependence. It is deploying automated tray assembly lines and digital tracking systems to “improve production efficiency and ensure that every step—from kitchen to boarding gate—delivers consistent quality and readiness.” Singapore’s SATS has implemented end‑to‑end digital monitoring modules covering meal assembly, cold‑chain management, and cabin cargo tracking, enhancing operational visibility and traceability.

At the more granular level of kitchen production, Middle Eastern aviation catering giant dnata is actively introducing smart cooking robots, substantially advancing its kitchen digitalisation to simultaneously improve operational efficiency and product quality. The digital factory is no longer just a technological concept; it has become a key driver for leading players to balance cost control and brand promise. The industry is rapidly polarising: leading players that can invest heavily in automation continuously strengthen their competitive moats by reducing labour dependence, lowering error rates, and shortening production cycles, while smaller players lacking such investment capabilities face considerable challenges.

Moreover, the digitalisation of onboard ordering is spreading rapidly. Passengers being able to pre‑select their meals via mobile apps has become an industry standard practice. This not only improves passengers’ sense of control over expectations but also helps airlines use predictive modelling to optimise load factors, thereby reducing food waste.

Greening and Operational Upgrades

Beyond fixed kitchen automation lines, the core logistics link that connects the kitchen to the aircraft door—the delivery fleet—is also undergoing profound technological upgrades. In 2025, LSG Sky Chefs invested $60 million to acquire a new fleet of 230 advanced delivery vehicles equipped with smart camera systems, collision avoidance systems, and optimised loading/unloading access. This significantly improves the efficiency and safety of the last‑mile delivery from kitchen to aircraft and lays the hardware groundwork for future integration into highly dynamic flight dispatching systems.

The transition to new energy is advancing in parallel. DO & CO became the first ground service provider in North America to operate fully electric refrigerated delivery vehicles at airports, reducing direct carbon emissions and fuel costs during apron operations. dnata is also advancing its electric delivery vehicle pilot programme and, in close cooperation with Mallaghan, is testing smart electric vehicles at multiple hubs, including London and Kuala Lumpur. In the Asia‑Pacific market, SATS’ regional business unit, Asia Airfreight Terminal, has reduced cumulative carbon emissions by 33% since 2018 through measures such as vehicle electrification, infrastructure upgrades, trial use of HVO green diesel, and switching to environmentally friendly refrigerants in its cold chain. It has set a target of fully electrifying its fleet by 2030. In addition, dnata has begun piloting AI‑based demand forecasting and onboard retail space‑loading optimisation modules, essentially pioneering the evolution of catering vehicles from “transport tools” into “mobile data nodes.”

Driving Factors

Global Air Traffic's Strong Recovery

The growth of in-flight catering services maintains a direct linear relationship with the increase in global air passenger numbers. According to the latest data from the International Air Transport Association (IATA), total global air passengers in 2025 are projected to reach 4.99 billion (approximately 5 billion). Although this forecast has been revised downward by 522 million from previous estimates due to global trade policy uncertainties and fluctuating consumer confidence, the 4% year-on-year growth rate still pushes passenger volumes significantly beyond pre-pandemic historical peaks. From a segment perspective, the recovery momentum of international routes has been notably stronger than that of domestic markets: international passenger demand grew by 7.1% year-on-year, while domestic passenger demand increased by 2.4%. The Asia-Pacific region led global growth with rates between 7.4% and 9%, establishing itself as the core engine of aviation recovery. At the operational level, the global passenger load factor for 2025 is expected to reach 83.6%-83.7%, with quarterly peaks surpassing 84%—hitting new historical highs. The full restoration of flight capacity and substantial increase in flight volumes mean that the dual growth in passenger throughput and sector operations directly translates into rigid in-flight meal demand, providing the most fundamental demand support for the industry.

The recovery of the aviation industry is reflected not only in passenger volumes but, more critically, in the continued improvement of airline profitability fundamentals, which brings a dual commercial benefit to the in-flight catering market. IATA forecasts that global airline net profits will reach 36 billion in 2025,as ignificant increase from 32.4 billion in 2024; the industry's net profit margin will rise from 3.4% to 3.7%, while passenger revenue will exceed $693 billion, setting a new historical record. The improvement in airline financial health creates a key transmission effect for the in-flight catering market: on the one hand, increased profitability directly unlocks airline budgets for meal services, particularly greatly expanding the scope for investment in premium and customised meals, thereby driving the transition of in-flight meals from "basic provision" to "quality upgrade." On the other hand, the divergence in regional airline profitability highlights the brand value of meals—Middle Eastern airlines lead globally with an 8.7% net profit margin, while European airlines achieve 4.3%. Leading regional airlines possess ample financial resources to leverage in-flight meals as a core tool for brand differentiation and service competitiveness, further activating market demand for premium and specialty meals.

Intensified Airline Competition: Meals as a Differentiator and Brand Tool

As the global aviation market recovers, industry competition has shifted from pure price wars to service differentiation. With its high perceptibility and customisability, in-flight catering is emerging as a core tool for airlines to build brand identity and enhance customer loyalty.

Facing intense fare wars, many airlines no longer view catering as a burdensome cost, but rather transform it into a tool for targeted monetisation and differentiation. For instance, Singapore Airlines, Emirates, and others have long reinforced their premium service positioning through high-end catering—chef partnerships, regionally inspired menus, and refined presentation. Meanwhile, in the low-cost carrier (LCC) segment, the competitive logic differs but similarly underscores the importance of catering. Airlines such as Ryanair and AirAsia leverage "buy-on-board" models, making meal products a core component of ancillary revenue.

Notably, Scandinavian Airlines (SAS) recently decisively abandoned its long‑held "New Nordic" concept, introducing the more inclusive and modular "Flavors by SAS" global concept to balance cost control with customisation. Air France and American Airlines have likewise expanded their "Buy‑on‑Board" (BoB) offerings, turning mini burgers, specialty snacks, and premium spirits into impulse‑purchase drivers. Transitioning from ticket sellers to lifestyle‑oriented onboard retailers, airlines are fishing for new profit growth in the red ocean through meticulously designed meals.

Airline Network Expansion and Long‑Haul Growth

The ongoing expansion of global airline networks and the rising share of long‑haul routes are magnifying in‑flight meal demand from both total volume and structural perspectives, driving steady growth in the onboard dining market. According to IATA data, global air passenger traffic is expected to reach 5.2 billion in 2026, up 4.4% year‑on‑year, with international route demand growing by 5.9%. Capacity expansion on long‑haul and ultra‑long‑haul routes is particularly pronounced.

Accelerated capacity recovery on long‑haul routes and their increased share mean that the meal value per flight is significantly higher than on short‑haul sectors. As OAG has noted, the continued growth in global air capacity is being driven by the recovery of long‑haul networks and strong performance in certain regional markets, sustaining post‑pandemic capacity increases. Citing OAG data, Aviation Week reported that global seat capacity in the third quarter of 2025 was 5.7% higher than in the same period of 2019. The Asia‑Pacific market, benefiting from the return of long‑haul demand and robust intra‑regional travel, has cemented its position as the world’s largest seat‑growth engine. On long‑haul flights, meals are not only served more frequently (typically multiple rounds, including full meals, light bites, and snacks), but passenger expectations for meal quality are substantially higher than on short‑haul flights, correspondingly driving supplier investments in cold‑chain logistics, menu planning, and premium ingredient sourcing, and further raising the overall value of in‑flight meals.

Global In-Flight Catering Services Market: Competitive Landscape

In terms of market concentration, the global industry remains moderately to highly concentrated with relatively stable competitive dynamics. The CR5 ratio remained around 58% in 2025 (58.44%), while the HHI index fluctuated between 7.78% and 8.23%, indicating that although the market is dominated by leading players, it has not reached full monopolistic concentration and still retains competitive fragmentation. Overall, the industry is characterized by a “leader-dominated but regionally dynamic” structure, with future concentration likely to remain stable but subject to localized redistribution driven by regional expansion, LCC growth, and digital capability differentiation. Key market participants include gategroup Holding AG, LSG Group, DO & CO Aktiengesellschaft, dnata, Newrest Group International, SATS Ltd., Flying Food Group, China Southern Airlines Group Air Catering Co., Ltd., China Eastern Air Catering Investment Co., Ltd., Cathay Pacific Catering Services (H.K.) Limited, ANA Catering Service Co., Ltd., Beijing Air Catering Co., Ltd, Air Culinaire Worldwide, JAL Royal Catering Co., Ltd, Chengdu Air Catering Co., Ltd., Cosmo Catering Co., Ltd., Guangzhou Baiyun International Airport, and Caissa Tourism Group.

Global In-Flight Catering Services Market: Market Segmentation Analysis

LSG Group

DO and CO Aktiengesellschaft

dnata

Newrest Group International

SATS Ltd.

Flying Food Group

China Southern Airlines Group Air Catering Co., Ltd.

China Eastern Air Catering Investment Co., Ltd.

Cathay Pacific Catering Services (H.K.) Limited

ANA Catering Service Co., Ltd.

Beijing Air Catering Co., Ltd

Air Culinaire Worldwide

JAL Royal Catering Co., Ltd

Chengdu Air Catering Co., Ltd.

Cosmo Catering Co., Ltd.

Guangzhou Baiyun International Airport

Caissa Tourism Group

Others

Market Segmentation (by Type)

Economy Class

Business Class

First Class

Market Segmentation (by Application)

Full-Service Carriers

Low-Cost Carriers

Others

Geographic Segmentation

North America

Europe

Asia-Pacific

South America

Middle East and Africa

Key Benefits of This Market Research:

• Industry drivers, restraints, and opportunities covered in the study

• Neutral perspective on the market performance

• Recent industry trends and developments

• Competitive landscape & strategies of key players

• Potential & niche segments and regions exhibiting promising growth covered

• Historical, current, and projected market size, in terms of value

• In-depth analysis of the In-Flight Catering Services Market

• Overview of the regional outlook of the In-Flight Catering Services Market:

Key Reasons to Buy this Report:

• Access to date statistics compiled by our researchers. These provide you with historical and forecast data, which is analyzed to tell you why your market is set to change

• This enables you to anticipate market changes to remain ahead of your competitors

• You will be able to copy data from the Excel spreadsheet straight into your marketing plans, business presentations, or other strategic documents

• The concise analysis, clear graph, and table format will enable you to pinpoint the information you require quickly

• Provision of market value (USD Billion) data for each segment and sub-segment

• Indicates the region and segment that is expected to witness the fastest growth as well as to dominate the market

• Analysis by geography highlighting the consumption of the product/service in the region as well as indicating the factors that are affecting the market within each region

• Competitive landscape which incorporates the market ranking of the major players, along with new service/product launches, partnerships, business expansions, and acquisitions in the past five years of companies profiled

• Extensive company profiles comprising of company overview, company insights, product benchmarking, and SWOT analysis for the major market players

• The current as well as the future market outlook of the industry concerning recent developments which involve growth opportunities and drivers as well as challenges and restraints of both emerging as well as developed regions

• Includes in-depth analysis of the market from various perspectives through Porter’s five forces analysis

• Provides insight into the market through Value Chain

• Market dynamics scenario, along with growth opportunities of the market in the years to come

• 6-month post-sales analyst support

Customization of the Report

In case of any queries or customization requirements, please connect with our sales team, who will ensure that your requirements are met.

Note: this report may need to undergo a final check or review and this could take about 48 hours.

Chapter Outline

Chapter 1 mainly introduces the statistical scope of the report, market division standards, and market research methods.

Chapter 2 is an executive summary of different market segments (by region, product type, application, etc), including the market size of each market segment, future development potential, and so on. It offers a high-level view of the current state of the In-Flight Catering Services Market and its likely evolution in the short to mid-term, and long term.

Chapter 3 makes a detailed analysis of the Market's Competitive Landscape of the market and provides the market share, capacity, output, price, latest development plan, merger, and acquisition information of the main manufacturers in the market.

Chapter 4 is the analysis of the whole market industrial chain, including the upstream and downstream of the industry, as well as Porter's five forces analysis.

Chapter 5 introduces the latest developments of the market, the driving factors and restrictive factors of the market, the challenges and risks faced by manufacturers in the industry, and the analysis of relevant policies in the industry.

Chapter 6 provides the analysis of various market segments according to product types, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different market segments.

Chapter 7 provides the analysis of various market segments according to application, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different downstream markets.

Chapter 8 provides a quantitative analysis of the market size and development potential of each region and its main countries and introduces the market development, future development prospects, market space, and capacity of each country in the world.

Chapter 9 introduces the basic situation of the main companies in the market in detail, including product revenue, gross profit margin, market share, product introduction, recent development, etc.

Chapter 10 provides a quantitative analysis of the market size and development potential of each region in the next five years.

Chapter 11 provides a quantitative analysis of the market size and development potential of each market segment (product type and application) in the next five years.

Chapter 12 is the main points and conclusions of the report.