Global Black Pellets Research Report 2025 (Status and Outlook)

Black pellets are an upgraded form of solid biomass fuel produced by subjecting raw materials such as wood residues, forestry by-products, and agricultural waste to thermochemical or physicochemical treatment, followed by densification into pellet form. Unlike conventional white pellets, black pellets undergo structural transformation during processing, which removes moisture and volatile compounds while increasing carbon content. The result is a fuel that behaves much more like coal in both handling and combustion. Its higher calorific value, resistance to water absorption, and improved grindability allow it to move through existing coal supply chains with minimal modification. This combination of properties positions black pellets as a practical bridge between traditional fossil fuels and low-carbon energy systems, particularly in sectors where full electrification remains difficult.

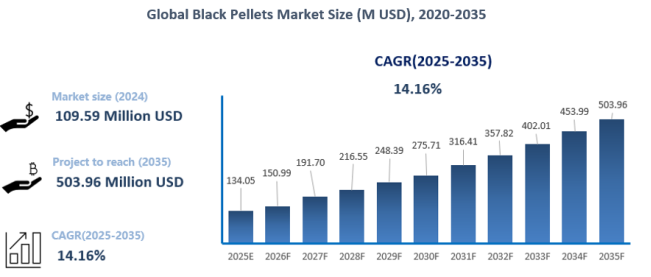

By 2024, the black pellets market had reached USD 109.59 million and is expected to expand at a CAGR of 14.16% from 2025 to 2035, reaching USD 503.96 million. This growth is primarily driven by the global energy transition, industrial decarbonization pressures, and supportive policy frameworks. As countries advance toward carbon neutrality, coal-fired power plants and industrial boilers face stricter emissions limits, creating strong demand for transitional fuels that can substitute coal at lower costs. Black pellets, with physical and combustion characteristics similar to coal, provide a strategic solution, enabling high co-firing ratios or full coal replacement without major infrastructure modifications, thereby significantly reducing capital expenditures for utilities. Policies such as carbon pricing, renewable mandates, and co-firing regulations further reinforce this demand by providing incentives and compliance pathways, enhancing market certainty. Advances in torrefaction technology have improved energy density, water resistance, and grindability, enabling efficient integration with existing coal systems, lowering production costs, and broadening feedstock options. Additionally, urgent energy security concerns and the abundant availability of agricultural and forestry residues support long-term market sustainability.

However, despite its growth potential, the black pellets market faces significant challenges across supply chain, technology, policy, and operational dimensions. High production costs—mainly due to capital-intensive torrefaction equipment and stringent feedstock quality requirements—limit price competitiveness, particularly in regions without mature carbon pricing mechanisms. Supply chain constraints, including the geographic dispersion of biomass, competition for raw materials, and limited transport radii, exacerbate cost and availability pressures. On the technology side, large-scale continuous production remains uncertain, with process stability and product consistency affecting end-user confidence, necessitating strict standardization. In downstream applications, retrofitting costs and energy system path dependencies hinder adoption, as industries already invested in alternative low-carbon solutions may resist switching. Policy dependence adds another layer of risk, as changes in subsidy programs, emissions regulations, and sustainability standards can directly impact demand. Operationally, the unique physical properties of black pellets create storage and self-heating risks, while the long certification cycles required by end users create a "chicken-and-egg" dilemma, slowing market expansion.

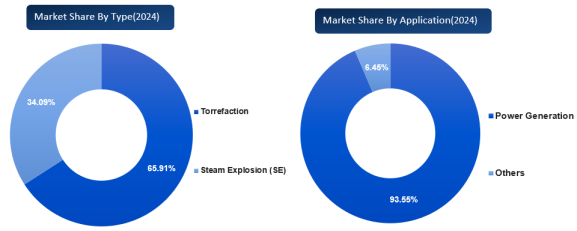

The black pellets market is primarily segmented by production technology, with Torrefaction and Steam Explosion (SE) representing the two dominant pathways. By 2024, torrefaction dominates the market with a 65.91% share, reaching USD 72.22 million, up from USD 23.48 million in 2020, reflecting its widespread adoption in power generation and industrial heating due to superior energy density and grindability. Steam explosion pellets are expected to account for 34.09% of the market in 2024, with a market size of USD 37.36 million, benefiting from cost-efficient processing and suitability for specific biomass conversion projects. Looking ahead, SE exhibits a slightly higher CAGR of 14.39%, suggesting that while torrefaction maintains sales leadership, SE is gradually gaining recognition as economies of scale and technological improvements enhance its competitiveness.

From an application perspective, the black pellets market is primarily driven by power generation, which accounted for 93.6% of total demand in 2024. Between 2020 and 2024, demand in power generation grew from USD 37.68 million to USD 102.52 million, reflecting rapid adoption for co-firing and industrial energy applications, supported by high energy density, compatibility with existing coal infrastructure, and favorable decarbonization policies.

Geographically, the market is highly concentrated in Europe, which accounted for 72% of the global market with USD 78.95 million in revenue in 2024. This reflects strong policy support for biomass co-firing, carbon reduction targets, and mature coal-fired power infrastructure compatible with torrefied pellets. The Asia-Pacific market, while smaller at USD 18.93 million (17.3%), is steadily growing due to rising industrial energy demand, government decarbonization initiatives, and the increasing adoption of advanced biomass technologies. North America contributed USD 7.46 million (6.8%), reflecting slower adoption due to limited policy incentives and competition from natural gas, but it is gradually expanding.

Black Pellets Industry Chain Analysis

Manufacturing Process Analysis of Black Pellets

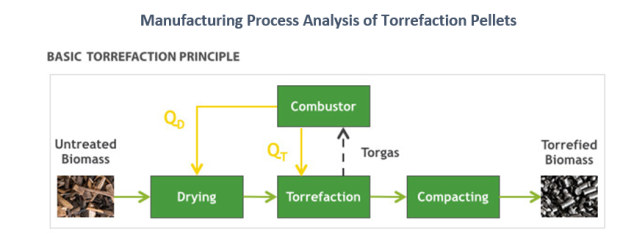

Biomass torrefaction is a thermal process used to produce high-grade solid biofuels from various streams of woody biomass or agro residues. The end product is a stable, homogeneous, high quality solid biofuel with far greater energy density and calorific value than the original feedstock, providing significant benefits in logistics, handling and storage, as well as opening up a wide range of potential uses.

Biomass torrefaction involves heating the biomass to temperatures between 250 and 300 degrees Celsius in a low-oxygen atmosphere. When biomass is heated at such temperatures, the moisture evaporates and various low-calorific components (volatiles) contained in the biomass are driven out. During this process the hemi-cellulose in the biomass decomposes, which transforms the biomass from a fibrous low quality fuel into a product with excellent fuel characteristics.

Typically the torrefaction process results in a mass loss (dry basis) of 20-30% and an energy loss of 10-15%. To make a biomass torrefaction plant economically viable it is crucial to use the energy “lost” in the volatiles. This can be done by burning the volatiles (torgas) in a lean gas combustor. This combustor can provide the heat for the drying and torrefaction. When the input feedstock has a moisture content of 35-45% the torrefaction process can be auto-thermal.

After torrefaction, the biomass raw material still has the problem of containing a large amount of alkali metal, which may corrode the reaction equipment. Therefore, further research can be done on the combination of roasting and other pretreatment technologies, with the purpose of further improving the characteristics of biofuels to facilitate the pyrolysis of biomass. For example, Saddawi et al. used washing pretreatment to reduce the alkali metal and chloride content of biomass, which improved the fuel properties after torrefaction. However, the combination of pretreatment technology will increase the cost, so it needs to be considered comprehensively.

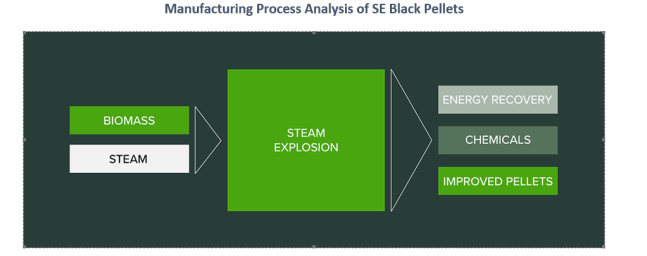

The steam explosion pretreatment technology is to realize the component separation and structural change of the raw material through the instantaneous pressure relief process under the action of high temperature (180-240 ℃) and high-pressure steam. This process can be completed by steam explosion equipment. This disrupts the rigid fiber structure, i.e. changes the chemistry. The energy density of ArbaCore black granules is equivalent to 76% of the energy value of coal. For conventional white wood pellets, this value is usually close to half the energy value of coal.

Development Trends

Black Pellet Fuel Is Gaining Increasing Attention

Renewable energy and carbon reduction policies in Japan, South Korea, Canada, Western Europe, and other countries support the use of pellet fuels as a replacement for coal in power plants. To date, investments in pellet fuel conversion have primarily focused on conventional industrial wood pellets, sometimes referred to as white pellets. According to Drax Group’s official 2024 annual report, the company’s biomass power generation business achieved a 27% year-on-year increase, generating 14.6 terawatt-hours (TWh), accounting for 10% of the UK’s renewable electricity. This data reflects the growing strategic value of biomass energy within the power system, and the high-performance form of biomass represented by black pellets is now being reconsidered for its market potential.

Although white pellets have already established large-scale trade networks in Europe and East Asia, their limitations in energy density, storage and transportation conditions, and combustion compatibility have gradually become key bottlenecks restricting further penetration. From a logistics and economic perspective, white pellets are bulky and have low energy density, resulting in transportation costs per unit of energy significantly higher than coal. This issue is especially pronounced in intercontinental trade (e.g., North America exports to Europe and Japan), directly eroding the cost advantage for power companies. Additionally, their hygroscopic nature requires strict dry storage conditions, further increasing infrastructure investment and operational complexity.

From a technical compatibility perspective, the chemical and physical differences between white pellets and coal make it difficult to co-fire high proportions in existing coal-fired power plants. Plants often require expensive boiler retrofits, and when using lower-quality wood (such as fast-growing species like eucalyptus), complete replacement of the combustion system may be necessary. Such high capital expenditure severely limits their large-scale substitution potential.

Against this backdrop, black pellets have emerged as an “upgraded biomass fuel.” Through torrefaction, they significantly enhance energy density, improve hydrophobicity, and increase grindability, making them more coal-like and enabling lower-cost integration into existing coal-fired systems. This “substitute upgrade” logic forms the most fundamental and certain growth driver of the black pellet market. Currently, the market is transitioning from early-stage technical validation and demonstration projects to large-scale commercialization. A key indicator of this shift is that major energy companies are signing long-term supply agreements and promoting upstream capacity construction, meaning market demand is no longer scattered pilot projects but predictable and sustainable procurement behavior.

Torrefaction Dominates, Steam Explosion Seeks Differentiated Breakthrough

Black pellet production technologies are primarily divided into two major camps, each exhibiting distinct commercialization trajectories. Torrefaction, due to its process maturity and product stability, currently dominates the market. According to a 2024 review published in the journal Energies, torrefaction treats biomass in an oxygen-deficient environment at 200–300°C, effectively removing moisture and volatile compounds, increasing energy density by 15–30%, significantly improving hydrophobicity, and making grindability close to coal. The main advantage of this technology is that it allows 20–30% co-firing ratios with existing coal infrastructure without major plant retrofits.

Blackwood Technology’s FlashTor® represents the torrefaction route, achieving commercial breakthroughs in Thailand. The FlashTor® facility, completed in 2024, has an annual capacity of 75,000 tons, processing wood and corn stover pellets, in partnership with TTCL and Eskom. The technology uses an indirectly heated rotary drum reactor to precisely control temperature and time, ensuring uniform torrefaction. Blackwood claims its process converts biomass into fuel with coal-equivalent calorific value, maintaining hydrophobicity and biodegradation resistance, suitable for long-term storage and long-distance transportation.

In contrast, steam explosion technology (SE) currently has a smaller market share but, due to lower production costs and unique fiber structure modification effects, is finding niche applications. The representative company Arbaflame in Norway has built the world’s largest single-capacity SE facility, with an annual output exceeding 200,000 tons. Its patented SE process produces fuel that can directly replace coal without co-firing. However, the pioneer Zilkha Biomass Energy went bankrupt in 2018, highlighting the technical risks of scaling this approach. In the future, these two technology routes may complement each other in different market segments: torrefaction dominating coal replacement in the power sector, and steam explosion serving higher reactivity needs in hydrogen gasification or biorefinery applications.

Driving Factors

Coal Replacement Demand and Industrial Decarbonization Pressure

The core driver of the black pellets market stems from the global energy system’s trend toward “de‑coalization.” As countries advance their carbon neutrality goals, traditional coal-fired power plants and industrial boilers face increasingly stringent emission constraints, while full replacement with intermittent renewable sources such as wind or solar remains unfeasible in the short term. During periods of unstable renewable generation—such as the wind power shortage caused by the European anticyclone in October–November 2024—biomass energy, capable of 24/7 power supply, becomes a critical infrastructure for grid stability. This creates rigid demand for transitional fuels that can “replace coal at low cost.”

In this context, black pellets exhibit clear strategic value: their physical and combustion properties closely resemble coal (high calorific value, good grindability), allowing direct co-firing or even full replacement in existing coal-fired systems, thereby avoiding extensive equipment retrofits. This compatibility substantially reduces capital expenditures (CAPEX) for utilities. Compared to conventional white pellets, which are typically limited to a 10% co-firing ratio and require costly modifications, black pellets can increase the co-firing ratio to over 30%.

Moreover, industrial sectors such as steel, cement, and chemicals rely heavily on high-temperature heat, making their decarbonization more challenging than the power sector. The rapid penetration of black pellets in industrial heating—the largest application segment—directly reflects this structural challenge. As emission constraints expand from power generation to industrial processes, demand is expected to continue strengthening.

Policy Support and Institutional Incentives

While the energy transition provides the “demand logic,” policy frameworks create the “institutional foundation” for accelerated black pellet market development. Governments in Europe, North America, and parts of Asia actively promote market expansion through direct and indirect mechanisms.

Carbon pricing mechanisms, including carbon taxes and emission trading systems, significantly raise the cost of coal, gradually making black pellets cost-competitive over their lifecycle. Simultaneously, policies such as mandated biomass co-firing ratios, renewable energy subsidies, and green electricity certifications create rigid demand. For example, some countries require coal-fired plants to use biomass at specific ratios, providing black pellets with a stable market entry point.

Importantly, policies are shifting from pure encouragement toward a combination of constraints and incentives. Stricter emission regulations are paired with subsidies, tax benefits, and long-term power purchase agreements (PPAs), lowering the cost of transition for enterprises. This dual approach transforms black pellets from an “optional solution” into a “compliance pathway,” significantly enhancing market certainty.

Technological Advancement

The emergence of black pellets as a superior alternative to traditional white pellets is fundamentally driven by torrefaction technology, which delivers a substantial performance upgrade. The technical feasibility of black pellets has been confirmed through rigorous scientific and engineering validation. According to a 2024 review published in ACS Energy & Fuels, torrefaction processes biomass in an oxygen-deprived environment at 200–300°C, markedly improving energy density, hydrophobicity, and grindability.

Specifically, torrefaction increases biomass energy density from approximately 18–19 MJ/kg to 20–24 MJ/kg, approaching coal-level calorific values. Hemicellulose degradation and reduced hydroxyl (O–H) groups confer hydrophobicity, enabling outdoor storage without moisture absorption. The removal of volatiles increases brittleness, reducing grinding energy consumption by 70–90%, with grindability comparable to coal. These physicochemical improvements allow co-firing at 20–35% in existing coal infrastructure (mills, conveyors, burners) without the 5–10% limitations of conventional wood pellets.

On the production side, torrefaction and related thermal processing technologies have been continuously optimized for efficiency, scalability, and feedstock flexibility, enabling the use of forestry residues, agricultural by-products, and energy crops. This not only lowers feedstock costs but also enhances supply chain flexibility. With ongoing standardization and scaling of equipment, unit production costs are expected to decline further, accelerating market penetration.

Global Black Pellets Market: Competitive Landscape

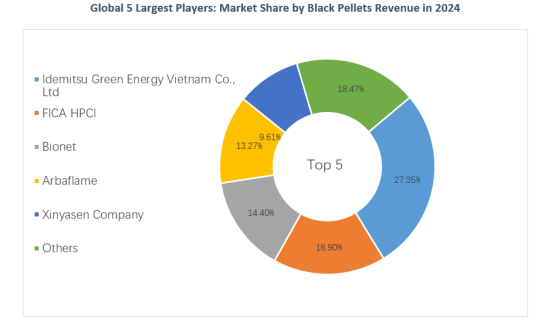

The global black pellets manufacturing sector exhibits a moderately concentrated market structure, dominated by a few major players. In 2024, the top five companies held a combined market share (CR5) of 81.53%, with a Herfindahl-Hirschman Index (HHI) of 15.10%, indicating moderate concentration and potential for increased competition as smaller players expand. By 2025, the market share of the top four companies is expected to decline slightly, suggesting a gradual dispersal of market dominance, with companies like Joensuu Biocoal entering the market. The key players in the black pellets market include Idemitsu Green Energy Vietnam Co., Ltd, FICA HPCI, Bionet, Arbaflame, Xinyasen Company, Blackwood Technology, Airex Energy, and Khodal Bio Fuel Company.

Global Black Pellets Market: Market Segmentation Analysis

The research report includes specific segments by region (country), manufacturers, Type, and Application. Market segmentation creates subsets of a market based on product type, end-user or Application, Geographic, and other factors. By understanding the market segments, the decision-maker can leverage this targeting in the product, sales, and marketing strategies. Market segments can power your product development cycles by informing how you create product offerings for different segments.

Key Company

Idemitsu Green Energy Vietnam Co., Ltd

FICA HPCI

Bionet

Arbaflame

Xinyasen Company

Blackwood Technology

Airex Energy

Khodal Bio Fuel Company

Others

Market Segmentation (by Type)

Torrefaction

Steam Explosion (SE)

Market Segmentation (by Application)

Power Generation

Others

Geographic Segmentation

North America

Europe

Asia-Pacific

South America

Middle East and Africa

Key Benefits of This Market Research:

• Industry drivers, restraints, and opportunities covered in the study

• Neutral perspective on the market performance

• Recent industry trends and developments

• Competitive landscape & strategies of key players

• Potential & niche segments and regions exhibiting promising growth covered

• Historical, current, and projected market size, in terms of value

• In-depth analysis of the Black Pellets Market

• Overview of the regional outlook of the Black Pellets Market:

Key Reasons to Buy this Report:

• Access to date statistics compiled by our researchers. These provide you with historical and forecast data, which is analyzed to tell you why your market is set to change

• This enables you to anticipate market changes to remain ahead of your competitors

• You will be able to copy data from the Excel spreadsheet straight into your marketing plans, business presentations, or other strategic documents

• The concise analysis, clear graph, and table format will enable you to pinpoint the information you require quickly

• Provision of market value (USD Billion) data for each segment and sub-segment

• Indicates the region and segment that is expected to witness the fastest growth as well as to dominate the market

• Analysis by geography highlighting the consumption of the product/service in the region as well as indicating the factors that are affecting the market within each region

• Competitive landscape which incorporates the market ranking of the major players, along with new service/product launches, partnerships, business expansions, and acquisitions in the past five years of companies profiled

• Extensive company profiles comprising of company overview, company insights, product benchmarking, and SWOT analysis for the major market players

• The current as well as the future market outlook of the industry concerning recent developments which involve growth opportunities and drivers as well as challenges and restraints of both emerging as well as developed regions

• Includes in-depth analysis of the market from various perspectives through Porter’s five forces analysis

• Provides insight into the market through Value Chain

• Market dynamics scenario, along with growth opportunities of the market in the years to come

• 6-month post-sales analyst support

Customization of the Report

In case of any queries or customization requirements, please connect with our sales team, who will ensure that your requirements are met.

Note: this report may need to undergo a final check or review and this could take about 48 hours.

Chapter Outline

Chapter 1 mainly introduces the statistical scope of the report, market division standards, and market research methods.

Chapter 2 is an executive summary of different market segments (by region, product type, Application, etc), including the market size of each market segment, future development potential, and so on. It offers a high-level view of the current state of the Black Pellets Market and its likely evolution in the short to mid-term, and long term.

Chapter 3 makes a detailed analysis of the Market's Competitive Landscape of the market and provides the market share, capacity, output, price, latest development plan, merger, and acquisition information of the main manufacturers in the market.

Chapter 4 is the analysis of the whole market industrial chain, including the upstream and downstream of the industry, as well as Porter's five forces analysis.

Chapter 5 introduces the latest developments of the market, the driving factors and restrictive factors of the market, the challenges and risks faced by manufacturers in the industry, and the analysis of relevant policies in the industry.

Chapter 6 provides the analysis of various market segments according to product types, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different market segments.

Chapter 7 provides the analysis of various market segments according to Application, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different downstream markets.

Chapter 8 provides a quantitative analysis of the market size and development potential of each region and its main countries and introduces the market development, future development prospects, market space, and capacity of each country in the world.

Chapter 9 details the production of products in major countries/regions and provides the production of major countries/regions.

Chapter 10 introduces the basic situation of the main companies in the market in detail, including product sales revenue, sales volume, price, gross profit margin, market share, product introduction, recent development, etc.

Chapter 11 provides a quantitative analysis of the market size and development potential of each region in the next five years.

Chapter 12 provides a quantitative analysis of the market size and development potential of each market segment (product type and Application) in the next five years.

Chapter 13 is the main points and conclusions of the report.