Market Insight- Global Combined Heat and Power (CHP) Market Overview 2025

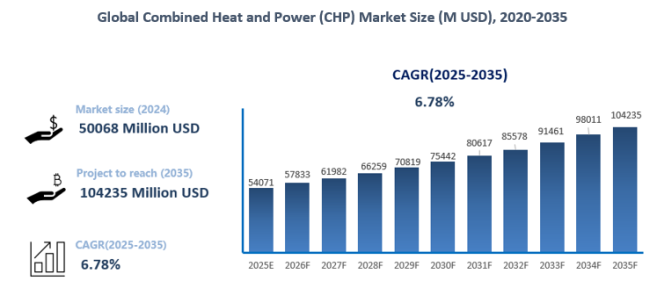

Global Combined Heat and Power (CHP) Market Was Valued at USD 50068 Million in 2024 and is Expected to Reach USD 104235 Million by the End of 2035, Growing at a CAGR of 6.78% Between 2025 and 2035.– Bossonresearch.com

Combined heat and power (CHP) equipment refers to integrated energy systems designed to generate electricity and capture usable thermal energy from a single fuel input at the point of consumption. By recovering heat that would otherwise be wasted in conventional power generation, CHP equipment achieves substantially higher overall efficiency, often reaching 70–90%, while also improving energy reliability and cost control. Typical systems combine prime movers such as gas engines, gas turbines, steam turbines, or fuel cells with generators, heat recovery units, and advanced control systems. These solutions can operate on natural gas, coal, biomass, industrial by-products, and increasingly low-carbon fuels, allowing them to be adapted to diverse regulatory environments and load profiles. As a result, CHP equipment is widely deployed across utilities, industrial plants, commercial buildings, and selected residential settings where stable heat demand supports continuous operation.

In 2024, the global CHP market reached USD 50,068 million, and it is expected to expand at a CAGR of 6.78% between 2025 and 2035, reaching USD 104,235 million by 2035. From a global perspective, CHP market growth is driven by a combination of energy transition pressures and real demand-side needs. Increasing requirements for energy system resilience and flexibility, coupled with grid instability and rising extreme weather risks, are prompting commercial and industrial users to adopt reliable on-site generation solutions. Simultaneously, clear policy frameworks, carbon reduction targets, and incentive mechanisms have elevated the economic and regulatory appeal of CHP, as its overall efficiency far exceeds that of conventional power generation. Technological advances further strengthen these drivers: improvements in engines, turbines, fuel cells, digital control systems, and hybrid integration with solar PV, energy storage, and microgrids enhance system performance, reduce lifecycle costs, and expand CHP applicability across various scales. Rapid urbanization and continued urban population growth also support long-term increases in heating demand across residential, commercial, and industrial sectors, particularly in emerging markets, creating a stable demand base for CHP deployment.

Amid global decarbonization and energy resilience trends, fuel reliance is gradually shifting from natural gas and coal to cleaner alternatives such as biogas, renewable natural gas, and hydrogen. This transition drives strong growth in small-scale modular CHP systems, especially in residential and commercial sectors, where end-users seek energy independence, lower utility costs, and reliable distributed power. Micro-CHP units further meet small-scale demand, offering flexible, low-emission solutions for homes, offices, and small industrial facilities. Hybrid microgrid systems combining CHP with solar PV and storage are increasingly adopted, enhancing reliability, grid independence, and carbon reduction potential, particularly for critical infrastructure. In high-end distributed energy applications, CHP continues to attract global attention due to its integrated cooling, heating, and power capabilities, delivering substantial efficiency, environmental, and economic benefits, with early adoption and operational experience in North America, Europe, and Japan.

At the same time, the CHP market faces key challenges from policy, economic, technological, and market constraints. While government support, feed-in tariffs, and carbon trading mechanisms have enhanced CHP attractiveness, the policy reliance on government guidance, regional disparities, and limited stability introduce significant investment uncertainty if regulations weaken or incentives change. Strict emission standards and grid connection regulations further raise market entry barriers, requiring higher compliance and technology upgrade investments, particularly in fuel switching and system retrofits, complicating economic evaluations. High initial capital costs, long payback periods, fuel price volatility, and electricity/heat market mechanisms that do not fully reflect system flexibility and value continue to pressure project profitability.

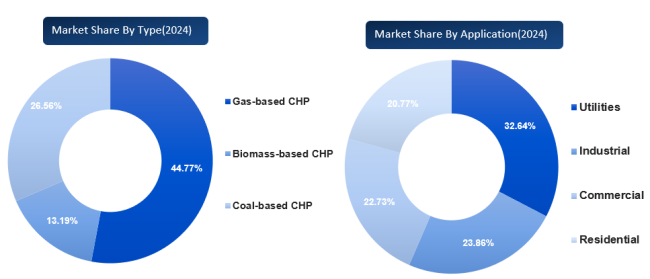

Segmented by type, Gas-based CHP dominated the 2024 market, accounting for 44.77% of revenue, reflecting its technical maturity and broad application across utilities, industrial, and commercial sectors. Its 2025–2035 CAGR of 7.01% is supported by stable fuel supply, regulatory incentives for efficiency, and the ability to integrate with renewable natural gas. Coal-based CHP, historically significant (26.56% share), is on a declining trajectory (-3.01% CAGR) due to stricter emission regulations, high carbon costs, and the global shift toward clean energy. The fastest-growing segments include hydrogen-based CHP (11.09% CAGR) and other emerging technologies (13.21% CAGR), reflecting the market’s shift toward low-carbon and flexible energy solutions, driven by technology breakthroughs, policy incentives, and growing decarbonization investments.

From an application perspective, the 2024 CHP market is led by utilities (32.64% share), reflecting dominance in large-scale energy production and regional district heating networks. Industrial CHP (23.86% share) shows the highest CAGR of 7.34%, benefiting from strong demand in energy-intensive industries such as chemicals, steel, and pharmaceuticals, where co-generation significantly improves operational efficiency and lowers costs. Commercial (22.73%) and residential (20.77%) sectors are smaller in scale but growing rapidly (6.91% and 7.23% CAGR, respectively).

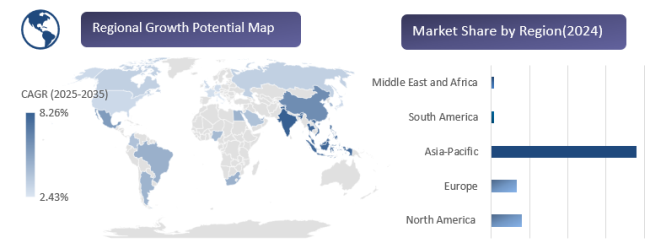

Geographically, the Asia-Pacific region dominates, with a 68.04% market share in 2024 and a projected 7.84% CAGR (2025–2035). This leadership stems from rapid industrialization, large-scale urbanization, and significant investment in district heating and industrial CHP projects, especially in China and India, where energy efficiency and emissions reduction are strategic priorities within a predominantly fossil-fuel-based energy structure.

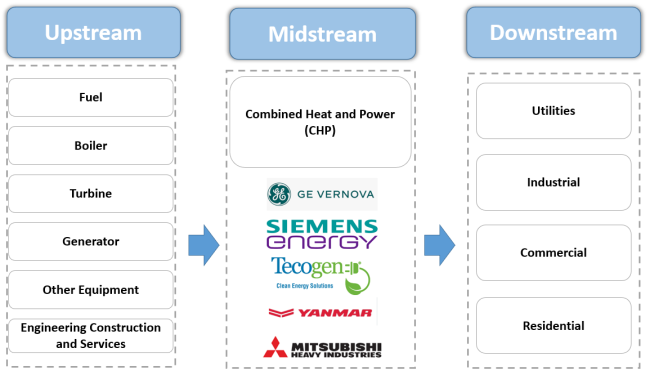

Combined Heat and Power (CHP) Industry Chain Analysis

Key Development Trends

Clean Fuels and the Shift Toward Decarbonization

Today, the most prominent trend in the CHP market is the increasing emphasis on decarbonization and reducing carbon emissions. With the global transition toward sustainable development and the urgent need to meet climate targets, CHP systems are under growing pressure to move away from traditional fossil fuel dependence and toward cleaner alternative energy sources. While traditional CHP systems have long relied on natural gas and, in some regions, coal as primary fuels, the market is clearly shifting toward renewable fuels. In particular, biogas, renewable natural gas (RNG), and hydrogen—fuels capable of significantly reducing the carbon footprint of CHP systems—are receiving increasing attention. For example, in Europe, COGEN EUROPE predicts that the share of renewable energy sources (RES) in CHP will exceed 64% in the near future.

Hydrogen-powered CHP systems (also referred to as “CHP 2.0”) are expected to grow rapidly in the coming years. By using 100% hydrogen as fuel, CHP systems can achieve higher efficiency while significantly reducing greenhouse gas emissions. For instance, Xi’an Xinkang in China has demonstrated that hydrogen-based CHP can raise the energy utilization efficiency of traditional fuel cells from 40% to over 95%. Hydrogen provides flexibility for future energy systems, particularly because it can be blended with other fuels such as natural gas, enabling existing infrastructure to transition to greener alternatives with minimal downtime. However, production, storage, and transport of clean hydrogen remain challenging, representing key barriers to widespread adoption in CHP that must be addressed.

The transition to clean fuels also aligns with broader energy transition strategies, which require the energy sector to demonstrate its ability to integrate with renewable energy. CHP systems can support distributed energy networks, such as microgrids, and complement solar, wind, and storage solutions. By using clean fuels and optimizing fuel efficiency, CHP systems will become an indispensable component of industrial decarbonization, district heating, and electricity generation, while also supporting broader energy transition goals set by governments worldwide.

Rising Demand for Small Modular CHP Systems

The market for small modular CHP systems is expanding rapidly, particularly in commercial and residential sectors. These systems range from 50 kW to several MW (e.g., Tecogen’s packaged CHP units) and are designed to meet the decentralized energy needs of end users. The main drivers of this trend are the demand for energy resilience, energy independence, and reduced utility costs. These systems are often factory-packaged and pre-fabricated for easy installation and operation, reducing the initial capital investment and complexity associated with traditional CHP. Additionally, publicly available product catalogs from institutions such as the U.S. Department of Energy facilitate comparison between systems, making it easier for small businesses to evaluate and implement CHP solutions. Their economic advantage lies in providing reliable energy, especially with black-start capability during emergencies.

From a market perspective, the growing demand for small CHP systems reflects the broader trend toward distributed generation within the global energy mix. With rising energy costs and increasing awareness of climate change driving the adoption of cleaner energy solutions, end users are increasingly turning to CHP as a reliable and flexible energy solution. This trend is particularly pronounced in North America and Europe, where the focus on energy efficiency and local grid independence is strong. Indeed, small CHP systems are expected to see significant growth in residential and commercial applications, driving overall expansion of the global CHP market.

Micro-CHP Systems

Micro-CHP systems (typically 1–50 kW) are another noteworthy trend in commercial and residential markets. These units provide small-scale energy solutions, often suitable for single-family homes, small businesses, and light industrial units. For buildings that require both electricity and heat but lack the space or budget for larger CHP units, micro-CHP systems are an ideal solution.

Micro-CHP systems offer numerous advantages, including fuel flexibility, low emissions, and high fuel conversion efficiency. They can utilize natural gas, biogas, or hydrogen and other renewable fuels. Companies like BlueGEN are leveraging fuel cell technology to advance micro-CHP systems. Beyond electricity generation, these systems contribute to grid stability through distributed generation, helping to alleviate congestion or reliability issues.

In commercial applications, micro-CHP units are increasingly adopted in office buildings, hotels, and retail spaces, where energy demands are relatively modest but operational reliability is critical. For small businesses, micro-CHP enables on-site heat and power generation, reducing energy costs while offering potential carbon emission reductions.

Driving Factors

Growing Importance of Resilience and Flexibility

The increasing demand for resilience and flexibility in energy systems has become one of the key drivers behind the expansion of the Combined Heat and Power (CHP) market. As global energy networks face mounting pressure from extreme weather events, natural disasters, and rising risks of grid failures, businesses and industries are seeking more reliable and independent energy solutions. CHP systems offer a highly valuable solution by continuing to supply both electricity and thermal energy even during grid outages.

These systems are designed to operate either independently (off-grid) or in parallel with the main grid, ensuring that critical energy needs—such as heating, cooling, and power generation—can be met even during power interruptions. This capability gives CHP systems a clear advantage in sectors where uninterrupted power supply is essential, including hospitals, data centers, and other critical infrastructure. In addition, enterprises located in regions with unstable grids are increasingly adopting CHP to mitigate outage risks and improve operational continuity.

Moreover, microgrid integration is emerging as a major trend in the CHP market, allowing small-scale distributed energy systems to connect to the main grid or operate autonomously. This flexibility ensures reliable energy supply regardless of grid instability, while enabling enterprises to optimize energy consumption and enhance overall system reliability.

Significant Untapped Technical Potential in Commercial and Industrial Sectors

The commercial and industrial sectors contain substantial untapped technical potential for the deployment and expansion of CHP systems. In recent years, these sectors have placed increasing emphasis on energy efficiency and sustainability, creating fertile ground for CHP adoption. This trend is particularly evident in energy-intensive industries such as manufacturing and processing, where recovering and utilizing waste heat for power generation can significantly reduce operating costs.

In industrial applications, CHP systems can be integrated into a wide range of manufacturing processes, including steel production, chemical processing, and food manufacturing. These industries typically require large and continuous supplies of both electricity and thermal energy, making CHP an ideal solution. By recovering waste energy, CHP systems not only reduce fuel costs but also help lower emissions by decreasing reliance on conventional energy sources. Similarly, in the commercial sector—such as office buildings, hotels, hospitals, and large mixed-use complexes—there is a growing preference for energy-efficient solutions to meet regulatory requirements and control energy expenditures.

Despite the growing adoption of CHP, a large portion of the market remains underdeveloped. Many buildings and facilities still rely on centralized grid electricity or inefficient heating systems. As government policies increasingly encourage decarbonization of energy systems, commercial and industrial applications present ample opportunities to adopt and benefit from advanced CHP technologies that simultaneously deliver power and thermal energy.

Increasing Focus on Energy Efficiency and Sustainability

With rising awareness of climate change, energy consumption, and environmental impacts, energy efficiency and sustainability have become core concerns for businesses, governments, and consumers alike. Governments around the world are paving the way for CHP market growth through strong policy instruments. These policies not only stimulate near-term demand but also shape a long-term market environment favoring high-efficiency, low-carbon technologies. For example, the EU’s Energy Efficiency Directive sets ambitious efficiency targets, the U.S. Inflation Reduction Act (IRA) provides tax credits for clean energy solutions including CHP, and China’s 14th Five-Year Plan for a Modern Energy System clearly defines development goals for CHP, offering a transparent roadmap for the industry. Such top-level policy frameworks provide stable long-term expectations for investors and enterprises.

The CHP market continues to grow due to its inherently high energy efficiency. In conventional power generation systems, a large share of energy is lost as waste heat and released into the environment. In contrast, CHP systems capture this waste heat for additional heating or cooling, significantly improving overall system efficiency. CHP systems can achieve efficiencies of up to 80–90%, compared with only 40–50% for traditional systems, making them highly attractive to industries seeking to reduce energy consumption and carbon emissions. By simultaneously producing electricity and heat, CHP systems reduce the need for separate energy generation units and optimize overall energy use within facilities.

Governments further encourage adoption of energy-efficient technologies through subsidies, tax incentives, and renewable energy support schemes. Policies that promote decarbonization and renewable integration are driving enterprises toward cleaner solutions such as CHP systems that can operate on biogas, biomethane, or even hydrogen. Ongoing carbon reduction commitments under international agreements such as the Paris Agreement further underscore the importance of energy systems that deliver reliable power while doing so in an environmentally responsible manner.

Global Combined Heat and Power (CHP) Market: Competitive Landscape

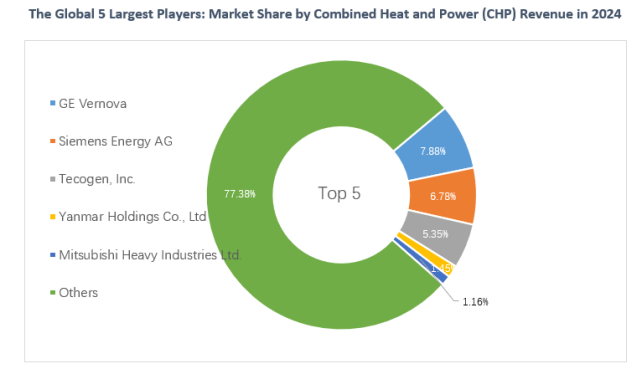

The global CHP Equipmentmarket shows moderate concentration, with the top five players holding a CR5 of 22.62% in 2024, projected to rise to 24.14% in 2025. GE Vernova and Siemens Energy are the leaders, contributing over 14% of the total market share. The HHI of 1.40% in 2024, increasing to 1.64% in 2025, indicates a relatively balanced competitive landscape, where no single firm dominates, but top manufacturers significantly influence technology standards, pricing, and large-scale project execution. Key manufacturers include GE Vernova, Siemens Energy AG, Tecogen, Inc., Yanmar Holdings Co., Ltd., Mitsubishi Heavy Industries Ltd., Everllence, Caterpillar, Bosch, Wartsila, Kawasaki Heavy Industries Ltd., Rolls-Royce Plc., Cummins Inc., Viessmann (Carrier), 2G Energy AG, Harbin Electric, Dalkia Aegis (EDF Group), Capstone Turbine Corporation, and Baxi Group (BDR Thermea).

Key players in the Combined Heat and Power (CHP) Market include:

Siemens Energy AG

Tecogen, Inc.

Yanmar Holdings Co., Ltd

Mitsubishi Heavy Industries Ltd.

Everllence

Caterpillar

Bosch

Wartsila

Kawasaki Heavy Industries Ltd.

Rolls-Royce Plc.

Cummins Inc.

Viessmann (Carrier)

2G Energy AG

Harbin Electric

Dalkia Aegis (EDF Group)

Capstone Turbine Corporation

Baxi Group (BDR Thermea)

Others

Request for more information

Click to view the full report TOC, figure and tables: https://bossonresearch.com/productinfo/1547548.html

About US:

Bosson Research (BSR) is a leading market research and consulting company, provides market intelligence, advisory service and market research reports for the automobile, electronics and semiconductor, and consumer good industry. The company assists its clients to strategize business policies and achieve sustainable growth in their respective market domain.

Bosson Research provides one-stop solution right from data collection to investment advice. The analysts at Bosson Research (BSR) dig out factors that help clients understand the significance and impact of market dynamics. Bosson Research (BSR) bring together the deepest intelligence across the widest set of capital-intensive industries and markets. By connecting data across variables, our analysts and industry specialists present our customers with a richer, highly integrated view of their world.

Contact US:

Tel: +86 400-166-9288

E-mail: sales@bossonresearch.com