Market Insight- Global Call Center Market Overview 2025

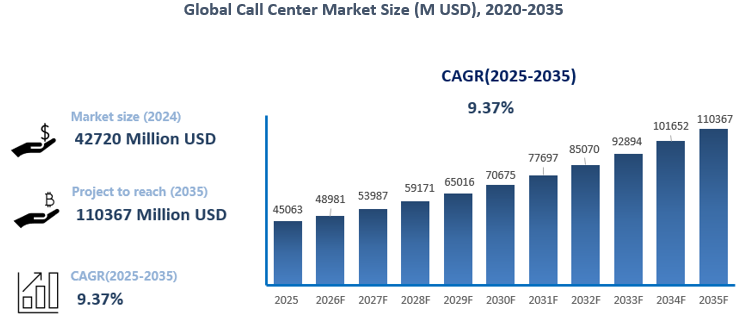

Global Call Center Market Was Valued at USD 42,720 Million in 2024 and is Expected to Reach USD 110,367 Million by the End of 2035, Growing at a CAGR of 9.37% Between 2025 and 2035.– Bossonresearch.com

The Call Center market is the global industry that provides the infrastructure, services, and technology enabling organizations to manage large volumes of customer interactions across multiple channels, including voice, email, chat, and social media. It encompasses inbound services such as customer support and technical assistance, as well as outbound services like telemarketing, sales, and collections. The market includes deployment models—cloud-based, on-premise, and hybrid solutions—along with software platforms such as CRM, automatic call distribution (ACD), interactive voice response (IVR), workforce management, and AI-driven automation. Market size is typically measured by revenue from services, software, and outsourced operations, segmented by industry served, deployment type, and geography, reflecting the total economic value of enabling efficient customer communication and engagement.

The call center market is undergoing a pronounced transformation, shifting from traditional on-premise setups to cloud and hybrid models, expanding from single-channel to omnichannel services, and extending its reach from mature markets to emerging economies. By 2024, the global market reached USD 42,720 million and is projected to grow at a CAGR of 9.37% from 2025 to 2035, reaching USD 110,367 million. This growth is fueled by technological advancement, rising industry demand, and global economic dynamics. Contact centers have evolved from cost-driven back-office functions into strategic growth engines, driven by rising customer expectations, increasingly complex inquiries, and the recognition that every interaction can enhance brand loyalty, revenue, and operational efficiency. AI integration, particularly large-model systems, has enabled human–machine collaboration, allowing machines to handle repetitive tasks while agents focus on complex and empathetic interactions, boosting productivity and customer satisfaction. Simultaneously, the surge in digital channels has created a need for omnichannel integration, enabling seamless, personalized experiences across voice, chat, social media, and apps, with predictive service emerging as the next frontier. Data-driven operations have become the foundation for decision-making, converting massive interaction data into actionable insights that optimize efficiency, sales, and retention. Geographic expansion continues as enterprises leverage offshore and nearshore outsourcing to balance cost, scalability, and service quality while coordinating global and local strategies.

Despite this momentum, the industry faces intricate challenges. Fragmented global compliance frameworks, such as GDPR, LGPD, and PIPL, drive higher infrastructure, monitoring, and operational costs and expose enterprises to severe penalties if not adhered to. AI adoption, while promising efficiency gains, remains incremental due to practical limitations in handling complex or emotionally charged interactions, uncertain ROI, and significant upfront investment. Rising data security and privacy risks further heighten operational pressure, particularly for multinational providers managing sensitive information across jurisdictions. Balancing globalized operations with localized adaptation and meeting growing demand for industry-specific customization remain strategic challenges.

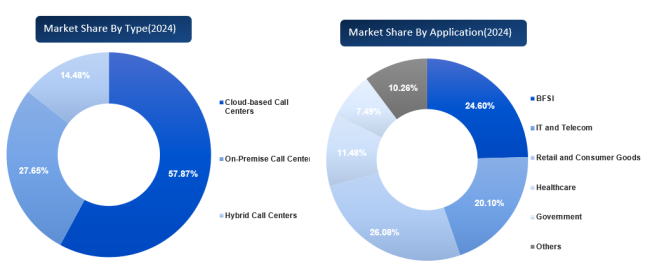

Cloud-based call centers have rapidly expanded due to their flexibility, scalability, remote management capabilities, and multi-channel integration, meeting 24/7 customer engagement needs and reducing infrastructure costs, accounting for 57.87% of the market in 2024 and projected to grow at a 10.22% CAGR through 2035. Hybrid models, though only 14.48% of the market in 2024, are expected to grow fastest at 12.78% CAGR, combining cloud agility with on-premise control. Sector-wise, Retail and Consumer Goods lead with 26.08% of the market, driven by omnichannel engagement and e-commerce growth, while BFSI holds 24.60%, relying on secure, high-volume, compliance-driven interactions. IT and Telecom grow fastest at 10.58% CAGR, reflecting strong reliance on digital and cloud services.

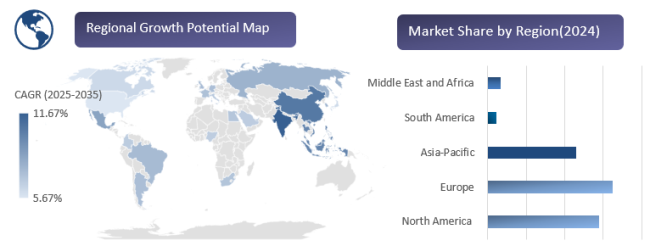

Regionally, Europe leads with USD 15,558 million in 2024 (36.42% global share) due to mature enterprises, demand for outsourced services, and advanced customer engagement technologies. North America follows with 31.83%, driven by multinational corporations and early adoption of cloud and hybrid models. Asia-Pacific, though smaller in absolute terms, is the fastest-growing region at 11.92% CAGR, fueled by rapid digital transformation, expanding BPO infrastructure, and demand for multilingual, scalable services.

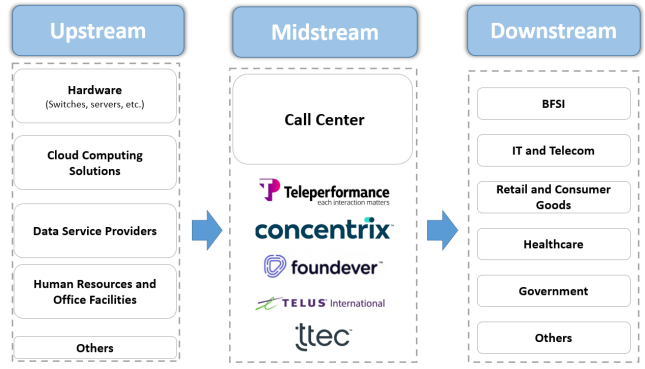

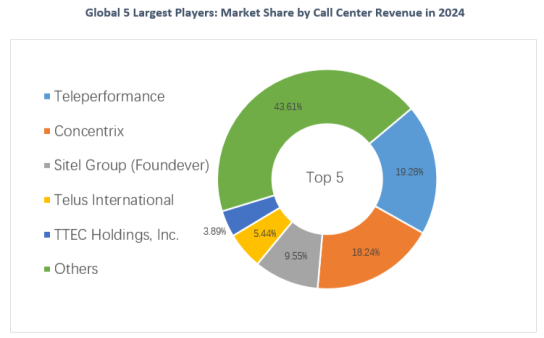

The global call center market is moderately to highly concentrated. The Herfindahl-Hirschman Index (HHI) is projected to rise from 7.08% in 2023 to 8.81% in 2025, reflecting increasing market concentration and competitive intensity. This trend indicates that strategic expansion, acquisitions, and technological differentiation by leading players are driving consolidation, while small and medium-sized enterprises face growing pressure to compete through specialization, innovation, or integration. Key market participants include Teleperformance, Concentrix, Sitel Group (Foundever), Telus International, TTEC Holdings, Inc., Alorica Inc., Atento S.A., Firstsource, Transcom WorldWide AB, TaskUs, EXL Service Holdings, Inc., Capita, Conduent Business Services LLC, Genpact, iSoftStone Information Technology, IBEX Limited, Serco Group Plc, TeleDirect Asia Pte Ltd. (TDCX), Intrado Life and Safety Inc., Nextiva Inc., PCCW Limited, Fusion CX, Hinduja Global Solutions (HGS), Open Access BPO LLC, Scicom, Entel Call Center SA, Callnovo Technology Co. Ltd., Sound Telecom, Connect Centre Pte Ltd., and Eureka Call Centre Systems Pte Ltd., etc.

Call Center Industry Chain Analysis

Key Development Trends

From Cost Center to Growth Engine

For a long time, call centers were widely regarded as a “cost burden” due to their heavy reliance on labor and technology investments, with core functions largely limited to issue resolution and complaint handling. In recent years, however, this perception has been fundamentally overturned. Jabra’s 2025 industry report clearly states that “the contact center in 2025 is no longer a cost center, but a growth engine—every customer interaction holds the potential to drive brand loyalty, empower employee performance, and improve business outcomes.” According to Qualtrics, 53% of customers say a single poor experience will cause them to reduce spending with a brand, an increase of 2.7 percentage points compared with 2024. At the same time, both the volume and complexity of customer inquiries continue to rise—Deloitte’s 2024 data show that 83% of customer experience leaders believe customer expectations are higher than ever before.

From a data perspective, the effectiveness of this transformation has already been quantitatively validated. McKinsey research indicates that AI-driven personalized services can increase customer satisfaction by 15–20%, lift revenue by 5–8%, and reduce service costs by as much as 30%. Mizuho Bank provides a representative case: by deploying a cloud-based, NLP-powered real-time analytics system, the bank dynamically identifies customer needs during live calls and provides agents with optimal response recommendations. This initiative not only shortened average interaction time by more than 6%, but also improved customer retention through more precise demand discovery—transforming the contact center from a pure service function into a core unit for deepening customer value.

This strategic upgrade is also reflected in the redefinition of organizational positioning. Traditionally, contact centers were typically housed under operations or customer service departments. Today, an increasing number of enterprises are elevating them to the group strategic level, with direct reporting lines to the CEO or CMO. This shift implies that the future core competitiveness of contact centers will no longer lie in “how many inquiries are handled,” but in “how much value is created.” Accordingly, performance metrics are moving away from operational indicators such as answer rates and average handling time toward value-based metrics including customer lifetime value, revenue contribution, and demand conversion efficiency.

Enhanced Human–AI Collaboration in Call Centers

The application of AI in contact centers has evolved from early-stage keyword matching and basic IVR systems to a deep empowerment phase centered on large language models. Unlike traditional AI, large-model-based intelligent systems possess capabilities such as contextual understanding, multi-turn dialogue, and emotional awareness, enabling a leap from “mechanical responses” to “human-like interaction.” Crucially, their core value lies not in replacing human agents, but in forming a collaborative and complementary relationship with them.

A representative example is the upgrade of Hangzhou Xiaoshan International Airport’s 96299 hotline—the first AI large-model-based intelligent call center in China’s civil aviation sector. Built on the DeepSeek large model, it established a “perception–decision–interaction” AI service framework, integrating advanced technologies such as affective computing and multimodal knowledge graphs. Semantic parsing accuracy reached 94.2%, with response efficiency improving by 300% compared with traditional systems. During peak periods such as large-scale flight delays, AI voice bots rapidly handle massive volumes of repetitive inquiries, increasing call answer rates from 83.8% to over 95% and reducing average waiting time from 15 seconds to just 3 seconds. Human agents, in turn, are freed to focus on scenarios requiring empathy and professional judgment, such as emotional reassurance and complex itinerary changes. This model—“AI handles standardized tasks, humans focus on high-value interactions”—improves service efficiency and customer satisfaction while reducing agent workload, achieving a win–win outcome.

It is worth noting that despite the growing adoption of AI, 75% of customers still prefer interacting with a human agent when dealing with complex or sensitive issues. Ambient AI tools can provide real-time guidance on tone, emotional cues, and escalation handling, helping agents manage emotionally charged interactions more effectively. For example, Hearing Care Central deployed AI-driven sentiment analysis and achieved a 30% increase in appointment bookings while conducting post-call cancellation surveys. The combination of real-time guidance and recognition mechanisms enhances agent confidence, well-being, and engagement, directly improving customer satisfaction and loyalty. A 2025 Calabrio study shows that although 98% of contact centers have deployed AI technologies, 61% of managers report rising complexity in customer conversations, largely because AI struggles with emotionally intense and ambiguous scenarios. This underscores that agents with strong empathy and complex problem-solving skills will become increasingly valuable, and that enterprises must strengthen soft-skill training alongside AI investments to build a dual-core service capability combining “intelligent efficiency” with “human warmth.”

Evolution Toward Channel Integration

As the digital economy advances, customer interaction channels have expanded from traditional phone calls to WeChat, SMS, social media, live streaming, and mobile apps, making channel fragmentation a core challenge for enterprises. Customers expect consistent and seamless service experiences when switching between channels, without having to repeatedly explain their needs or verify their identities. Investment in unified agent desktops and omnichannel routing engines enables enterprises to manage interactions across multiple channels without relying on siloed tools. This not only shortens handling time but also improves cross-channel context retention, allowing agents to deliver more personalized and efficient service.

True omnichannel integration is not about simply adding more channels, but about intelligent collaboration built on a unified platform. A representative case is Black Box’s solution for a rapidly expanding logistics startup in India. Facing challenges such as the absence of physical infrastructure, fragmented customer data, and a geographically dispersed workforce, the company needed to rapidly build a customer service system covering 300 delivery hubs. By deploying a Genesys cloud contact center integrated with Simple CRM, Black Box enabled centralized management of phone, SMS, and app-based interactions. Agents gained access to a unified workspace with a 360-degree customer view, allowing them to seamlessly continue service regardless of the customer’s previous channel, without requiring repeated information. This solution not only enabled infrastructure-light global service collaboration, but also improved service quality and agent productivity through process automation and data centralization, accelerating market expansion.

Looking ahead, omnichannel integration will evolve toward “predictive service.” By integrating customer data across channels and applying AI algorithms to analyze behavioral patterns and preference signals, contact centers can anticipate customer needs and provide proactive service before customers initiate contact. For example, if a customer checks logistics information in an app multiple times without reaching out, the system can automatically push shipment updates via SMS or trigger a proactive outbound call. This proactive service model is set to become the next core phase of omnichannel integration, further enhancing customer engagement and brand affinity.

Driving Factors

Escalating Competition in Customer Experience (CX) and Structural Shifts in Service Demand

The most fundamental—and most enduring—growth driver of the contact center market stems from a broad shift in corporate competitive logic from “products and price” toward “customer experience (CX).” In most mature industries, rising product commoditization and steadily increasing customer acquisition costs (CAC) have pushed enterprises to focus more heavily on extracting value from existing customers (LTV). In this context, service quality directly influences customer retention, repeat purchases, and brand loyalty, transforming contact centers from back-office support functions into core front-end customer touchpoints.

As customer expectations continue to rise, enterprises face a structural change in service pressure. Customers are no longer satisfied with simply being able to reach customer service; they now demand faster response times, higher first-contact resolution (FCR) rates, and more consistent cross-channel experiences. As a result, contact centers are evolving beyond basic inbound handling systems into comprehensive service platforms that integrate process management, knowledge management, and unified customer history.

At the same time, the nature of customer interactions themselves is changing. Early contact centers primarily handled standardized inquiries such as billing questions or basic information requests. Today, an increasing share of interactions involves complex complaints, personalized solutions, technical support, and emotional reassurance. These high-complexity interactions significantly increase the business value of each engagement and amplify the impact of service quality on customer decision-making, prompting enterprises to continuously increase investment in their contact center ecosystems.

Outsourcing and Strategic Partnerships

Outsourcing remains a powerful engine of enterprise growth, as companies seek access to specialized capabilities without building them entirely in-house. Third-party call center service providers possess deep expertise in workforce management, technology integration, compliance infrastructure, and multilingual service delivery, enabling enterprises to scale rapidly and innovate more effectively.

Strategic partnerships with technology vendors—such as CCaaS providers or AI solution companies—allow enterprises to adopt new capabilities quickly without incurring substantial internal R&D costs, further accelerating growth. These partnerships often foster co-innovation, with vendors embedding AI, analytics, and workforce engagement tools into standardized service offerings that continuously evolve in response to market demand. This model enables enterprises to achieve operational flexibility and ongoing feature upgrades without heavy capital investment in infrastructure, directly linking costs to growth outcomes.

Moreover, contact center growth is no longer driven solely by call volumes, but increasingly by value-added services, ecosystem partnerships, and layered capability offerings. This allows enterprises to expand their service portfolios while controlling costs and complexity. The rising demand for value-added service expansion among enterprises is therefore providing an additional boost to overall market development.

Global Delivery and Expansion into Emerging Markets

The ongoing restructuring of global industrial and supply chains, coupled with the accelerating international expansion of Chinese enterprises and multinational corporations, has become a core structural driver of growth in the call center and contact center market. As production networks, sourcing bases, and end markets become increasingly dispersed, enterprises face growing complexity in managing cross-border customers, partners, and after-sales interactions. This has led to a sharp increase in demand for scalable, cross-border customer service and operational support capabilities.

Meanwhile, emerging economies are becoming more deeply integrated into global production and supply chain networks, particularly in industries such as manufacturing, electronics, automotive, and industrial equipment. As these economies move up the value chain, manufacturing enterprises are increasingly adopting service-oriented business models, expanding after-sales support, technical assistance, lifecycle management, and customer engagement services. This “servitization of manufacturing” significantly increases both the volume and complexity of customer interactions that must be supported on a global scale.

Consequently, enterprises now require contact center capabilities that operate across regions, time zones, and channels to support geographically dispersed customers, suppliers, and partners. Demand is rising not only for traditional customer service, but also for technical support, order coordination, warranty management, and supply chain communication—often delivered in multiple languages and subject to diverse regulatory regimes. As a result, contact centers are evolving into critical infrastructure nodes that connect global production with global consumption.

Global Call Center Market: Competitive Landscape

The global call center market is moderately to highly concentrated. The Herfindahl-Hirschman Index (HHI) is projected to rise from 7.08% in 2023 to 8.81% in 2025, reflecting increasing market concentration and competitive intensity. This trend indicates that strategic expansion, acquisitions, and technological differentiation by leading players are driving consolidation, while small and medium-sized enterprises face growing pressure to compete through specialization, innovation, or integration. Key market participants include Teleperformance, Concentrix, Sitel Group (Foundever), Telus International, TTEC Holdings, Inc., Alorica Inc., Atento S.A., Firstsource, Transcom WorldWide AB, TaskUs, EXL Service Holdings, Inc., Capita, Conduent Business Services LLC, Genpact, iSoftStone Information Technology, IBEX Limited, Serco Group Plc, TeleDirect Asia Pte Ltd. (TDCX), Intrado Life and Safety Inc., Nextiva Inc., PCCW Limited, Fusion CX, Hinduja Global Solutions (HGS), Open Access BPO LLC, Scicom, Entel Call Center SA, Callnovo Technology Co. Ltd., Sound Telecom, Connect Centre Pte Ltd., and Eureka Call Centre Systems Pte Ltd., etc.

Key players in the Call Center Market include:

Concentrix

Sitel Group (Foundever)

Telus International

TTEC Holdings, Inc.

Alorica Inc.

Atento S.A.

Firstsource

Transcom WorldWide AB

TaskUs

EXL Service Holdings, Inc.

Capita

Conduent Business Services LLC

Genpact

iSoftStone Information Technology

IBEX Limited

Serco Group Plc

TeleDirect Asia Pte Ltd. (TDCX)

Intrado Life and Safety Inc.

Nextiva Inc.

PCCW Limited

Fusion CX

Hinduja Global Solutions (HGS)

Open Access BPO LLC

Scicom

Entel Call Center SA

Callnovo Technology Co. Ltd.

Sound Telecom

Connect Centre Pte Ltd.

Eureka Call Centre Systems Pte Ltd.

Request for more information

Click to view the full report TOC, figure and tables: https://bossonresearch.com/productinfo/1547548.html

About US:

Bosson Research (BSR) is a leading market research and consulting company, provides market intelligence, advisory service and market research reports for the automobile, electronics and semiconductor, and consumer good industry. The company assists its clients to strategize business policies and achieve sustainable growth in their respective market domain.

Bosson Research provides one-stop solution right from data collection to investment advice. The analysts at Bosson Research (BSR) dig out factors that help clients understand the significance and impact of market dynamics. Bosson Research (BSR) bring together the deepest intelligence across the widest set of capital-intensive industries and markets. By connecting data across variables, our analysts and industry specialists present our customers with a richer, highly integrated view of their world.

Contact US:

Tel: +86 400-166-9288

E-mail: sales@bossonresearch.com